A late-filing penalty for a US LLC does not depend on the profits earned. This can therefore become very expensive, particularly when a company has not generated any profit, because there are form and reporting obligations. In addition to the IRS penalties for failures, there are also numerous other ones. This guide therefore covers the following topics:

Read on to learn more so you are properly prepared and can protect yourself from sometimes very high penalty payments.

Your LLC’s late-filing penalties become due because of the information and filing obligations. For that reason, substantial failure payments are possible even if very little has happened operationally. Incorrect or incomplete data can even be treated as “not filed”.

A prominent example is, for instance, a US LLC owned by non‑US residents from Germany failing to submit Form 5472 on time. This triggers a base penalty of USD 25,000 and possible additional penalties if the breach continues despite an IRS notice. Interest is also charged with a compounding effect.

IRS penalties for a US LLC are divided into two broad categories:

While the IRS uses fixed amounts within this logic for some LLC structures, other models involve different calculation methods. Some penalties can even be avoided. Learn more about this in the next sections.

Avoid expensive late-filing penalties quickly with a professional law firm.

A key factor in determining a late-filing penalty is how the business is classified. For an LLC, different forms, deadlines and penalties apply depending on whether it is treated as a non-separate tax entity (“disregarded entity”), a partnership (“partnership”), with an S‑Corp election (“s‑corp election”) or a C‑Corp election (“c‑corp election”).

These are imposed partly as a fixed amount, per month, or as a percentage of the tax due. Penalties for information and filing obligations apply regardless of profit, while for payment obligations late-payment penalties usually relate to the tax liability.

These should be distinguished from the general flat-rate IRS penalties, most recently for example USD 60, USD 130 and USD 340. These apply to certain information returns, such as Form 1097, Form 1098, Form 1099, Form 3921, Form 3922, Form 5498 and Form W‑2G.

In the next section you will find an overview of late-filing penalties by LLC model, including the most important documents, the different filing deadlines and the calculation models used for late-filing penalties. However, this is only an overview. Each case should be reviewed individually and no form should be overlooked.

Save time and money now with an interdisciplinary team of experts.

If the single-member LLC is controlled by non‑US residents (“nonresidents”), potential late-filing penalties must be considered even with no turnover. This is because, even without the need for an income tax return, filing Form 1120 and Form 5472 with the IRS may still be required.

Form 5472 must be filed by the 15th day of the 4th month after the end of the tax year. If the date falls on a weekend or holiday, the deadline moves to the next business day. If Form 5472 is not filed or is incomplete, a base penalty of USD 25,000 applies. If no proper filing is then made, a further USD 25,000 is imposed every 30 days.

If you formed the US LLC from Germany and it is classified as a “foreign-owned U.S. disregarded entity”, electronic filing may be restricted. In that case, in practice you will usually have to submit Form 5472 and the pro forma 1120 by mail or fax. It is important that all reportable transactions are included.

For US residents, the classic IRS late-filing guideline applies. They must file Form 1040 on time. Otherwise, for failure to file, a penalty of 5% per month applies up to a maximum of 25%. For failure to pay, it is 0.5% per month up to 25%. Longer delays lead to a minimum penalty of USD 525.

In addition to the primary late-filing penalties for a single-member LLC, penalties can arise for other ignored or inaccurate forms. These include, among other things, US nexus and payments to foreign persons such as Form 1042 and 1042‑S. For payments to employees, forms such as Form 941, 940, W‑2, W‑3 and others are also required.

Consult specialists now for a compliant US tax return.

A multi-member LLC is treated like a partnership and must file Form 1065 as well as Schedules K‑1, K‑2 and K‑3 including any extensions. These must be filed by the 15th day of the 3rd month after the end of the tax year. For a calendar year, this is 15 March, with the deadline moving to the next business day if it falls on a weekend.

For a multi-member LLC, the late-filing penalty is assessed per partner and per month. In this context, penalties are possible for a period of up to 12 months. In 2025, Form 1065 incurred USD 245 per partner per month. The formula is: amount x number of partners x months.

In addition, a further late-filing penalty may apply for late or incorrect partner statements such as Schedule K‑1. In this case, under IRS instructions, USD 340 per statement is due. However, depending on the company size there is a cap.

Further documents may also be relevant for a multi-member LLC to avoid penalties. For example, if amounts are withheld as withholding tax, section 1446 may become relevant. Depending on the payment flows, Forms 1042, 1042‑S and 1099 may also be relevant. Payroll obligations such as Forms 941, 940, W‑2 and W‑3 must also be observed.

Safeguard your multi-member LLC tax return against risks now.

The LLC with an S‑Corp election generally applies only to US residents, apart from exceptions such as trusts. The penalties relate to the owners and the months, with up to 12 months counted. In 2025, a late Form 1120‑S (due on the 15th day of the 3rd month) resulted in USD 245 per partner per month.

If there is a tax liability, additional components may apply. For example, for failure to file it is generally 5% per month, and for failure to pay 0.5% per month, with both capped at 25%; in the latter case, interest may also apply. For very late filing of more than 60 days, the IRS even imposes a minimum penalty of USD 525.

There are additional IRS penalties for an LLC with an S‑Corp election. If the K‑1, K‑2 and K‑3 statements are filed late or incorrectly, further late-filing penalties of USD 340 per document apply. If done wilfully, at least USD 660 or 10% of the reportable amount is due. The maximum is USD 4,098,500, or USD 1,366,000 for small LLCs.

For an LLC with an S‑Corp election, the information returns system may also be relevant for payments to service providers. For example, 1099‑NEC would then be required. Likewise, for employees the forms Form 941, 940, W‑2 and W‑3 must be considered to avoid incompleteness and penalties.

Avoid risky mistakes on Form 1120‑S now with experts.

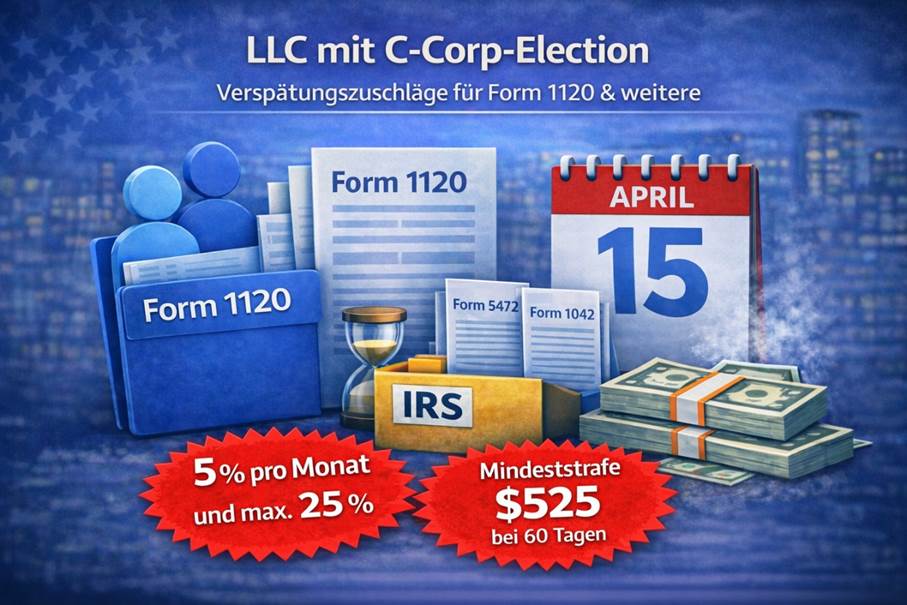

For an LLC with a C‑Corp election, the IRS imposes a late-filing penalty if Form 1120 is filed late and payment is made after the 15th of the 4th month of the tax year. For a calendar year, that is 15 April. If the date falls on a weekend, the filing deadline moves to the next business day. After 60 days, the minimum penalty is USD 525.

The failure penalty for an LLC with a C‑Corp election is typically set as a percentage for failure to file and failure to pay. Because it is calculated at 5% per month up to a maximum of 25%, the late-filing penalty can be relatively low. However, penalty payments can increase due to interest and compounding.

For an LLC with a C‑Corp election, several other documents may become mandatory. If it is controlled by foreign entities, Form 5472 including recordkeeping requirements becomes important. Also relevant are withholding cases with Forms 1042 and 1042‑S, payments to US contractors with 1099, and various payroll forms.

Do not miss any key documents now with an expert team.

Document | Required by | Due date | Penalty (Failure to file) |

Form 5472 | Single-member LLC, C‑Corp | 15/04 (calendar year; otherwise the 15th day of the 4th month after tax year end) | USD 25,000 (per violation; +USD 25,000 for each additional 30 days after IRS notice) |

Form 1120 | Single-member LLC, C‑Corp | 15/04 (calendar year; otherwise the 15th day of the 4th month after tax year end) | 5%/month on tax due, max. 25% (for pro forma with 5472 often USD 0 tax due; main penalty is usually via Form 5472) |

Form 1065 | Multi-member LLC | 15/03 (calendar year; otherwise the 15th day of the 3rd month after tax year end) | USD 245–255 per partner/month (adjusted annually; max. 12 months) |

Form 1120-S | S‑Corp | 15/03 (calendar year; otherwise the 15th day of the 3rd month after tax year end) | USD 245–255 per shareholder/month (adjusted annually; max. 12 months) |

Schedule K-1 | Multi-member LLC, S‑Corp | 15/03 (with Form 1065/1120‑S; later if an “extension” applies) | Up to USD 340 per statement (depending on lateness; if intentional disregard, min. USD 680) |

Schedule K-2 | Multi-member LLC, S‑Corp | 15/03 (with Form 1065/1120‑S; later if an “extension” applies) | Up to USD 340 per statement (depending on lateness; if intentional disregard, min. USD 680) |

Schedule K-3 | Multi-member LLC, S‑Corp | 15/03 (with Form 1065/1120‑S; later if an “extension” applies) | Up to USD 340 per statement (depending on lateness; if intentional disregard, min. USD 680) |

Form 1099-NEC | Single-member LLC, Multi-member LLC, S‑Corp, C‑Corp | 31/01 (recipient copy + IRS; follow e‑file rules) | Up to USD 340 per return/statement (depending on lateness; if intentional disregard, min. USD 680) |

Form 1099-MISC | Single-member LLC, Multi-member LLC, S‑Corp, C‑Corp | 31/01 (recipient copy); IRS: 28/02 paper / 31/03 e‑file | Up to USD 340 per return/statement (depending on lateness; if intentional disregard, min. USD 680) |

Form 1042 | Single-member LLC, Multi-member LLC, S‑Corp, C‑Corp | 15/03 (annually; calendar year) | 5%/month on withholding/tax due, max. 25% (special rules may also apply for withholding) |

Form 1042-S | Single-member LLC, Multi-member LLC, S‑Corp, C‑Corp | 15/03 (annually; calendar year) | Up to USD 340 per return/statement (depending on lateness; if intentional disregard, min. USD 680) |

Form 8804 | Multi-member LLC | 15/03 (often together with Form 1065; section‑1446/withholding context) | 5%/month on withholding due, max. 25% (statement penalties may also apply) |

Form 8805 | Multi-member LLC | 15/03 (statement to foreign partner; usually together with 1065/8804) | Up to USD 340 per statement (depending on lateness; if intentional disregard, min. USD 680) |

Form 8813 | Multi-member LLC | 15/03 (withholding/payment voucher in the 1446 context; per case) | 5%/month on withholding due, max. 25% (special rules may also apply) |

Form 941 | Single-member LLC, Multi-member LLC, S‑Corp, C‑Corp | 30/04, 31/07, 31/10, 31/01 (quarterly; last day of the following month) | 5%/month on tax due, max. 25% (deposit penalties may also apply) |

Form 940 | Single-member LLC, Multi-member LLC, S‑Corp, C‑Corp | 31/01 (annually) | 5%/month on tax due, max. 25% (deposit penalties may also apply) |

Form W-2 | Single-member LLC, Multi-member LLC, S‑Corp, C‑Corp | 31/01 (to employees + SSA) | Up to USD 340 per form (depending on lateness; if intentional disregard, min. USD 680) |

Form W-3 | Single-member LLC, Multi-member LLC, S‑Corp, C‑Corp | 31/01 (to SSA; summary of W‑2) | Up to USD 340 per form (depending on lateness; if intentional disregard, min. USD 680) |

Form W-4 | Single-member LLC, Multi-member LLC, S‑Corp, C‑Corp | — (onboarding/change) | No direct standard penalty (risk: incorrect payroll withholding/deposits) |

Form W-9 | Single-member LLC, Multi-member LLC, S‑Corp, C‑Corp | — (before/at vendor onboarding) | No direct standard penalty (missing/incorrect TIN can trigger backup withholding & 1099 penalties) |

Form 1040 | Single-member LLC, Multi-member LLC, S‑Corp, C‑Corp | 15/04 (as a rule; weekend/holiday rule may apply) | 5%/month on tax due, max. 25% (minimum penalty possible if >60 days) |

Form 1040-NR | Single-member LLC, Multi-member LLC, S‑Corp, C‑Corp | 15/04 (often; sometimes 15/06 depending on the case) | 5%/month on tax due, max. 25% (minimum penalty possible if >60 days) |

Form 1041 | Single-member LLC, Multi-member LLC, S‑Corp, C‑Corp | 15/04 (calendar year; otherwise the 15th day of the 4th month after tax year end) | 5%/month on tax due, max. 25% (additional penalties may apply for info statements) |

Form 7004 | Single-member LLC, Multi-member LLC, S‑Corp, C‑Corp | 15/03 or 15/04 (must be filed by the regular due date of the respective main return) | No direct penalty (must be filed on time; otherwise the penalty for the main return applies) |

Form 4868 | Single-member LLC, Multi-member LLC, S‑Corp, C‑Corp | 15/04 (by the regular due date of 1040/1040‑NR) | No direct penalty (only effective if filed on time; payment deadline still applies) |

Form 8809 | Single-member LLC, Multi-member LLC, S‑Corp, C‑Corp | 31/01 or 15/03 (depending on the information return; request must be filed by the relevant due date) | No direct penalty (only effective if filed on time; otherwise information-return penalties apply) |

Form 8832 | Single-member LLC, Multi-member LLC, S‑Corp, C‑Corp | — (before effective date; limited retroactive effect possible) | No direct penalty (risk: incorrect entity status → penalties for the wrong returns) |

Form 2553 | Single-member LLC, Multi-member LLC, S‑Corp, C‑Corp | 15/03 (calendar year; rule: no later than 2 months + 15 days after the start of the tax year) | No direct penalty (risk: election ineffective → wrong return types & penalties) |

BOI Report | Single-member LLC, Multi-member LLC, S‑Corp, C‑Corp | Depends on the formation date (deadlines under CTA/FinCEN; rules may change) | Civil penalty per day possible (amount per current FinCEN rule; wilful breach can be criminal) |

Form 3537 | Single-member LLC, Multi-member LLC, S‑Corp, C‑Corp | 15/04 (California; “extension” payment voucher for LLC) | State-specific (especially interest/penalties may apply for late payment) |

Resolve your US tax return quickly and professionally now.

Although FinCEN (Financial Crimes Enforcement Network) has excluded domestic US entities and persons since March 2025 via an Interim Final Rule, reporting relating to BOI (Beneficial Ownership Information) is still partly relevant.

For example, foreign reporting companies and therefore legal forms such as GmbH, Ltd. and offshore companies may still be subject to reporting. This is the case when they are registered in a US state and intend to do business there.

If companies registered before 26/03/2025, filing was generally due by 25/04/2025. For registrations after 26/03/2025, filings become due within 30 calendar days after the registration takes effect.

CTA penalties assume intent. This leads to civil late-filing penalties of up to USD 591 per day, with amounts adjusted for inflation. Criminally, they can mean up to USD 10,000 and/or up to 2 years’ imprisonment.

However, there is also a safe-harbour rule in this context. It applies if incorrect information is provided within a defined window, usually 90 days. But sanctions can be waived only if the incorrect reporting was not wilful.

Protect yourself from all late-filing penalties now with an expert team.

In addition to late-filing penalties from the IRS and BOI, further penalties may apply in the various US states. Below you will therefore find an overview of the respective failure penalties:

State | Required document (LLC) | Cycle / due date | Standard fee | Late fee / special feature |

California | Franchise Tax + Statement of Information | Franchise Tax: annually (depending on registration date) / SOI: every 2 years (end of anniversary month) | USD 800 + USD 20 | USD 250 penalty for SOI failure to file |

Delaware | Annual Tax (LLC) | annually, 1 June | USD 300 | USD 200 penalty + 1.5%/month interest |

Florida | Annual Report | annually, 1 May | USD 138.75 | USD 400 late fee |

Georgia | Annual Registration | annually, 1 April | USD 50 online / USD 60 paper | USD 25 late fee |

Montana | Annual Report | annually, 15 April | sometimes waived before the deadline / after the deadline USD 35 | USD 35 after the cut-off date |

Nevada | Annual List + Business Licence Renewal | annually, end of anniversary month | USD 150 + USD 200 | USD 100 penalty (business licence) + USD 75 default penalty (annual list context) |

Texas | Franchise Tax Report (as a “report/equivalent”) | annually, 15 May | USD 0 (below revenue threshold, in this overview) | Min. USD 50 penalty (late report; depending on the case) |

In other US states, late-filing penalties may not apply, or the LLC may instead be dissolved as a penalty due to unpaid fees.

Don’t overlook any factors now with interdisciplinary expert teams.

If you are now concerned about a possible late-filing penalty, there are still ways to prevent it. Below you will learn the common options with which you may still be able to avert a significant penalty payment.

For the different classifications of a US LLC, Form 7004 can be used to obtain extensions (“extension”) of 6 months. Depending on the structure, this relates to Form 1120 for a single-member LLC treated as a disregarded entity, to Form 1065 for a multi-member LLC, to Form 1120‑S for an LLC with an S‑Corp election, and to Form 1120 for an LLC with a C‑Corp election.

The extension request via Form 7004 must be filed with the IRS on time by the regular due date of the relevant tax return. This can be done in writing or electronically via e‑filing. However, it should be noted that the payment deadline still applies.

Another way to avoid late-filing penalties is to claim reasonable cause. In this context, you must have acted with ordinary care and prudence. If it was still not possible to file the tax return with the IRS on time, this can be mitigating.

While ignorance is not a defence, typical reasons for reasonable cause include:

IRS late-filing penalties can also be avoided via relief under FTA (“First Time Abate”). However, this relief applies only to certain standard penalties such as failure to file, failure to pay and failure to deposit.

This option can also apply to partnership and S‑Corp filing penalties. The condition, however, is a clean compliance history for 3 years. Some penalties, such as failure to pay, may still continue until full payment is made.

Get advice now on avoiding late-filing penalties.

Secure a free initial consultation

Often yes, because for a US LLC it is not only tax payment but, above all, reporting and filing obligations that matter. This is particularly the case as soon as there are reportable transactions with the owner and related parties.

Yes. In addition to the IRS, further late-filing penalties from various US states and, in some set-ups, BOI/CTA can be relevant, especially for foreign reporting companies. Besides late-filing penalties, interest and administrative consequences can also occur.

For a US LLC, an extension is filed via Form 7004, and for individual returns usually via Form 4868. This allows the filing deadline to be pushed back by a further 6 months. However, this does not automatically extend the payment deadline as well.

Ideally, IRS penalties are avoided by filing a timely extension request using Form 7004 or Form 4868. In addition, even for an LLC run carefully and prudently, there can be reasonable causes that are accepted, such as illness and technical problems. First Time Abate can also help with standard penalties under certain conditions.

For late or incomplete filing, Form 5472 incurs penalties of USD 25,000 (and potentially a further USD 25,000 every 30 days). For Form 1120 and 1040, failure to file is usually 5% per month up to 25%, and failure to pay is often 0.5% per month up to 25% plus interest. For 1065 and 1120‑S, late-filing penalties apply per partner/shareholder, per month and per person.

You need a sound baseline documentation set covering structure, owner(s), transactions, bank and bookkeeping data, and clear supporting evidence. For Form 5472 in particular, the transaction allocation and documentation logic are critical, while 1065 and 1120‑S require partner and shareholder data for K‑1 and potentially K‑2 and K‑3 as well.

Form 1065 is typically needed for a multi-member LLC without a corporate election, Form 1120‑S for an LLC with an S‑Corp election, and Form 1120 for an LLC with a C‑Corp election. The documents, deadlines and penalty logic depend on the specific classification of the limited liability company.

In addition to the main return such as Form 1065, 1120‑S, 1120 and 5472, supplementary documents are usually required. For foreign matters, these can include Schedules K‑1, K‑2 and K‑3, or 1099 forms for reportable payments to US service providers. Various documents for payroll, withholding and employees may also apply, such as Forms 940, 941, W‑2 and W‑3, and for payments to foreign persons Forms 1042 and 1042‑S.

The date for a calendar year can vary depending on the year, the rules, and weekends and holidays. For Form 1065 and Form 1120‑S it is usually 15 March, and for Form 1120, Form 5472 and the pro forma Form 1120 it is predominantly 15 April.

Form 5472 is a tax form for reportable transactions between the US entity and foreign related parties. Typically, Form 5472 is filed together with a pro forma Form 1120, and all transactions must be documented completely and coherently due to the recordkeeping requirements.